The cryptocurrency market lost more than half of its peak value. Total capitalisation has contracted to $2.37 trillion, the lowest level in 12 months and about 52% below the high of $4.38 trillion reached in October 2025. But to read the market as a homogeneous monolith on the way down would be an analytical error: what is happening is a sharp separation between assets, strategies and infrastructure, a rotation that rewards those who have built real moats and penalises those who have lived by narratives.

Bitcoin is at the centre of this bifurcation. While it has fallen significantly from its highs, it has held on a relative basis compared to the altcoin universe, with capital preferring to move into it rather than remain in the smaller tokens. The comparison is brutal: the median token in the non-bitcoin market has lost about 79% since its peak in late 2024, according to Pantera Capital. Bitcoin is approaching one of the worst first-quarter performances since 2018, but the Crypto Fear and Greed index hitting 5, coupled with Google Trends’ data on “crypto” searches at annual lows, could indicate exhaustion of retail selling pressure rather than further deterioration. Whether the current level holds will depend on how quickly the macro picture changes and whether institutional ETF inflows hold.

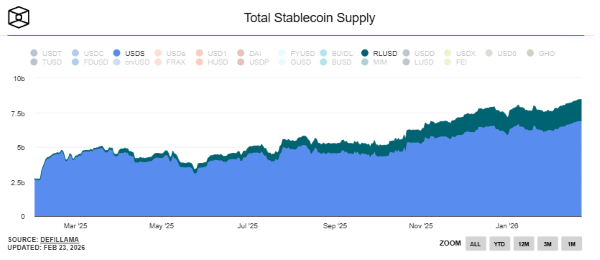

In this context of generalised compression, the stablecoin market tells a completely different story, and deserves separate attention. Sky Protocol’s USDS reached a new record high of around 6.9 billion units, growing 48% year-on-year, with over $290 million in additional supply in the last month alone. The trajectory is no coincidence: Sky has been systematically working on institutional expansion, including the launch of Keel as an on-chain capital allocator with a $500m campaign to attract Real World Asset issuers to Solana, and the entry of Morpho Vault as a curator. In parallel, Ripple’s RLUSD surpassed 1.5 billion in offerings on 20 February, starting from just 83 million a year ago, and is now approaching the 2 billion mark. The difference from other stablecoins is structural: RLUSD operates under a New York DFS charter with bank-level supervision, Ripple has conditional approval by OCC charter, and the recent listing on Binance has created the liquidity infrastructure needed to scale with institutional desks. The message is clear: in a market that squeezes speculative values, stablecoins with yield or regulatory differentiation attract flows that would otherwise stop.

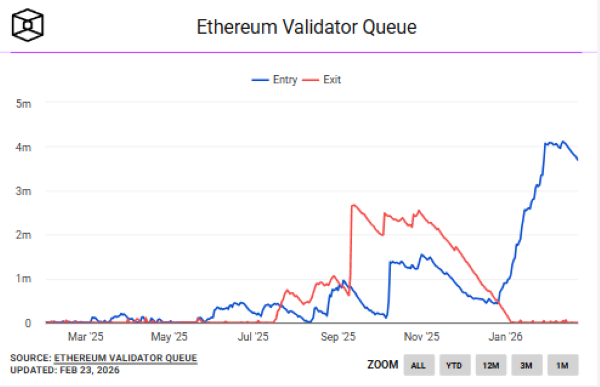

On the Ethereum front, the most significant figure this week is not the price, but the validator queue: more than 4 million ETHs awaiting activation with a lead time of more than 60 days, the highest staking demand since 2023. Simultaneously, the exit queue is close to zero, whereas in September 2025 it was at 2.67 million ETH. Thirty per cent of the circulating supply of ETH is now staked, a structural level that reduces the supply available to the market. Part of this demand comes from institutional hoarding: BitMine holds about 4.37 million ETH, or 3.6 per cent of the circulating supply, with a stated goal of increasing to 5 per cent. SharpLink, the second largest corporate treasury ETH, holds about 867,000 ETH with almost no planned exits. And BlackRock has started seeding its iShares Staked Ethereum Trust (ETHB), with a target share of 70-95% of staked assets for an estimated annual return of 3%, expected to launch in the first half of 2026.

The most disruptive event of the week on the infrastructure front, however, is the divorce between Base and Optimism. Coinbase announced that Base will abandon the OP stack and migrate to its unified code base (Base/Base), ending three years of dependency and, most importantly, redefining its fee streams. Base generated more than 90 per cent of Superchain’s revenue. The Optimism Collective had just approved a governance proposal to allocate 50% of the sequencer’s revenues to the monthly repurchase of OP tokens, a value accumulation mechanic now stripped of its premise. The market responded ruthlessly: OP plummeted about 36% in a few days, hitting a new all-time low at $0.14, marking -97% from its 2024 all-time high. The Layer 2 GML2 index has lost 75% in the last 12 months.

In the background, a potential sign of renewed speculative appetite emerged from Pump.fun: the token graduation rate exceeded 1.05%, the highest level since July 2025, with three days above 1% in February for the first time in seven months. The new Cashback Coins mechanism, which forces creators to choose between retaining commissions or redistributing them to traders irreversibly, is changing the alignment of incentives on the platform.

What the February 2026 market is really saying is this: liquidity has shifted to three types of assets – proven value stocks like Bitcoin, stablecoins with real yield or compliance, and ETH locked in institutional validators with multi-year horizons. Everything else is burning. This is not pessimism: it is natural selection, and the market does this job better than any analyst.