The cryptocurrency market seems to have reignited its engines. Three key indicators bear witness to this: the explosive return of blue-chip NFTs, the soaring value of options on Bitcoin and the increasing adoption of cryptos as balance sheet assets by listed companies. An explosive cocktail pushing the sector towards a new maturity of structured finance, corporate transactions and true institutional asset class dynamics.

Let’s start on the NFT front, where CryptoPunks are back to laying down the law. With weekly trading volume of over $24.6 million, the highest since March 2024, the collection saw a 416% increase over the previous week. The floor price rose from 40 to 47.5 ETH and the average selling price hit $182,000. Behind this boom is GameSquare, Nasdaq-listed company and mother of the FaZe Clan, which invested $5.15 million in preferred shares to buy Punk #5577, an extremely rare ‘Punk Bee’. Not just marketing: this is the first time a public company has used equity to acquire an NFT, treating it as a balance sheet asset capable of generating returns. A strong signal for funds, treasuries and high-end collectors: top-tier NFTs can be strategic financial instruments.

On the corporate side, the market is witnessing a paradigm shift. The aggregate capitalisation of public companies holding cryptocurrencies rose from $90 billion to $165 billion in 2024, with share performance in double digits after every crypto buyout announcement. The use of metrics such as mNAV (multiple net asset value) has made it possible to assess the real impact of these digital assets on balance sheets. But the most intriguing aspect concerns the big token holders: instead of selling in the market and causing bearish pressure, they are transferring their cryptos to these companies in exchange for equity, exploiting the liquidity of traditional markets. It is an ingenious ploy: treasuries become exit strategies disguised as advanced financial strategies. All very elegant, but also incredibly clever.

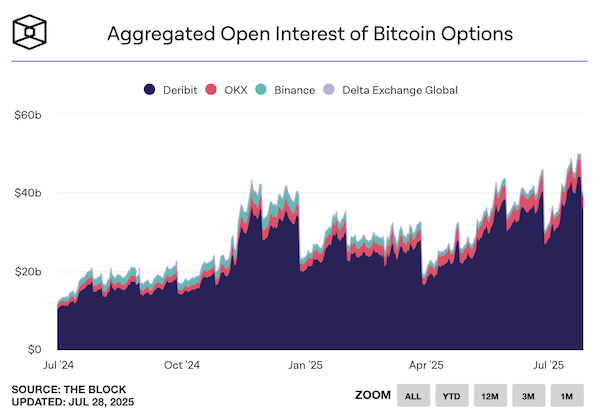

Then there is the world of derivatives, where interest in Bitcoin options has reached almost $50 billion, with Deribit controlling around $45 billion. Add to that the 7 billion in the ETF universe, such as IBIT options. Coinbase, which acquired Deribit for $2.9 billion in May, now enjoys a dominant position in a market that attracts both retail and institutional traders. In parallel, Ethereum continues to benefit from this speculative and institutional wave, consolidating its central role in derivatives markets and treasury strategies.

The hunger for sophisticated instruments such as options is no longer a niche. It has become a necessity for miners, hedge funds and companies that want to manage exposure without liquidating assets. So the question is no longer ‘whether’ cryptos are mature. The question is: who will be next to treat them as digital gold?