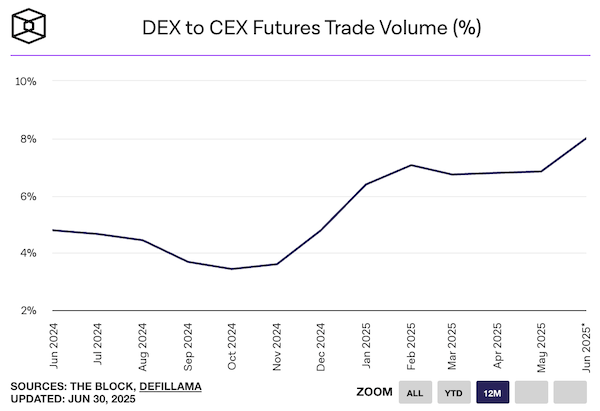

There is a new wind blowing in the crypto markets and, although it has not yet become a storm, it is being felt loud and clear in trading volumes, fees collected and new balances in derivatives trading. Driving the change is the impressive growth in the ratio of futures volumes in DEX to CEX, which reached 8% in June 2025 alone. Never had such a level been reached, a clear sign of a decentralisation that is taking shape not just as an ideological narrative, but as a concrete reality in market numbers.

Driving this growth is Hyperliquid, which alone generated over $210 billion in perpetual futures volume in June. A figure down 15% from the previous month, yes, but one that appears extraordinary when compared to Binance, which lost 20% over the same period. This differential pushed the Hyperliquid/Binance ratio to a new high of 11.3%, confirming the relative strength of the decentralised protocol. Also contributing to the trend was APX Finance, now merged with Astherus under the Aster brand, which, with over USD 34 billion in volume, posted a 350% month-on-month increase, driven by aggressive incentive programmes. The data speak for themselves: DEXs are no longer the nerdy cousin of CEXs, but are becoming key players in a scene where trust is increasingly on-chain.

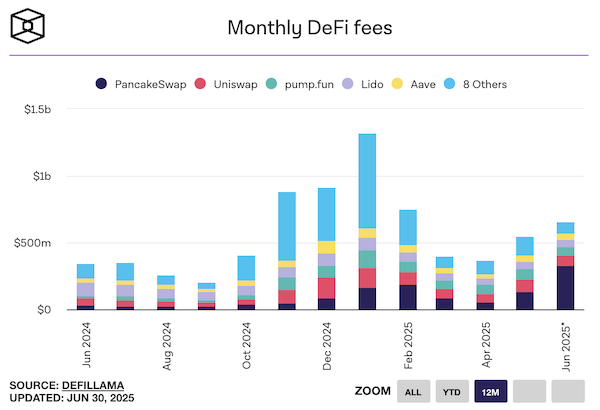

And if volumes tell the tale of change, revenues confirm its sustainability. After months of decline, DeFi’s protocols are returning to profitability. Total monthly fees are now around USD 577 million, a 58% rebound from the April low. This recovery coincides with a new phase of vitality in decentralised platforms, fuelled by growing volumes and increasingly refined business models. PancakeSwap, for example, dominates the scene with over $275 million in fees, followed by Uniswap and lending protocols such as Aave and MakerDAO that manage to cash in through interest and liquidation penalties.

What makes the difference is DeFi’s ability to offer peer-to-peer solutions without intermediaries, cutting costs and raising margins. The protocols not only survive, but evolve: they optimise fees, build user loyalty, and manage to generate value even in highly volatile ecosystems such as memecoins, where Pump.fun stands out for the frequency of transactions that, though small, add up to significant volumes. A new decentralised economy is emerging, which monetises in an organic and disintermediated manner, increasingly less dependent on the traditional banking environment.

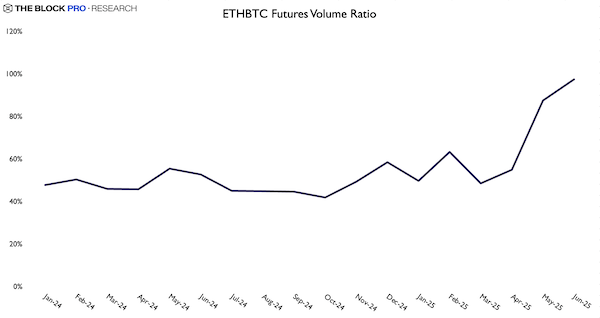

But the most disruptive change is not only measured in volumes or balance sheets. It can be perceived in the power relations that govern the hierarchies between the major cryptocurrencies. The ratio of Ethereum futures volumes to Bitcoin volumes has risen to 98 per cent, virtually on par. A figure that seems to be coming out of another cycle compared to the autumn of 2024, when Ethereum seemed destined for a structural decline, stifled by high fees, fierce competition and regulatory uncertainty. Today, Ethereum is breathing again, buoyed by the spread of Layer 2s, rising DeFi activity and a narrative that sees it once again as a hub of innovation.

Meanwhile, Bitcoin continues to be the markets’ solid institutional anchor, but its dominance is beginning to creak under the weight of new expectations. With the arrival of ETFs on Solana and XRP, the derivatives scenario becomes even more competitive. But Ethereum has on its side a mature ecosystem, an established developer base, and a technological advantage that could prove decisive in the new phase of institutional adoption.

Those who only look at absolute numbers risk missing the sense of direction. What is happening is not just a summer bounce or a momentary change of preferences. It’s a redefinition of the rules of the game, where DEX are finally on a par with CEX, DeFi is generating profits like a solid company, and Ethereum is really starting to bite Bitcoin’s heels. If there is one truth in crypto markets, it is that nothing stays the same for too long. And this time, the revolution is not asking for permission: it is entering through the front door, with volumes, fees and futures in hand.